As a real estate legal professional, you deal with risk on your clients’ behalf every day. They count on you to help them navigate the real estate process and make sure their home or business has the coverage it needs. You work hard to help protect them and their interests. But how are you protecting yours?

Real estate is the riskiest area of law

Real estate and litigation have formed the bulk of claims every year since LawPRO started releasing annual reports in 1995. In over half of the reports, claims from real estate practices were higher than litigation claims. Here’s why:

Mistakes happen

Client expectations are always rising, and they want deals to be closed faster than ever. There’s only a minor chance of human error on any one component of a deal, but even straightforward deals have many moving parts.

The complexity of real estate transactions is one of the major reasons that title insurance is such important protection for clients. Every element of the deal has a small chance of an error, and it only takes one to cause a loss.

Real estate errors and omissions are expensive

Real estate transactions deal with hundreds of thousands, often millions of dollars in value. Even a mistake that causes a small percentage error can result in a significant real loss.

Property prices have been on the rise for the last decade, and their growth has only accelerated in the past few years. Even in this current climate with house prices cooling, the stakes of practicing real estate law are much higher than they used to be.

Why your mandatory insurance isn’t enough

The errors and omissions (E&O) insurance provided through your law society is a great baseline of protection, but it has limits and can end up costing you.

Having to make a claim through your law society’s indemnity insurance could result in your premium going up, and depending on the deductible, you may only get partially reimbursed for your loss. The key is to supplement your mandatory insurance by working with experts.

At FCT, we know about managing risk. That’s why we’ve developed a suite of insurance products designed to help legal professionals enhance their mandatory E&O coverage.

Deal Protection Endorsement

The Deal Protection Endorsement is an add-on for residential purchase and refinance transactions title insured with FCT. It insures your client directly for errors or omissions on your part that don’t fall under the protection of their title insurance policy (in B.C., it insures the lawyer or notary themselves), up to the total value of the policy itself.

It provides you the same peace of mind that your title insured client enjoys. It can cover claims in the millions of dollars, and applies to the title insurance policy, not your mandatory or FCT E&O insurance. That means claims covered by the endorsement never count against your E&O claims limits.

FCT E&O Extra®

E&O Extra is automatically applied to every purchase or refinance transaction you title insure with us, at no extra cost—all you need to do is register. If you make a claim to your mandatory E&O insurance because of a title insured deal, and you’re registered for E&O Extra, we cover the deductible and any increases to your premiums.

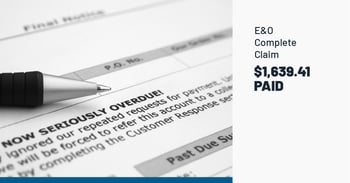

FCT E&O CompleteTM

Use E&O Complete to keep small mistakes from becoming big problems. For a low annual premium, you can submit up to three claims per calendar year related to purchase, refinance or sale transactions directly to FCT.* You don’t need to go through your mandatory E&O insurance, and the error doesn’t need to have resulted in legal action.

The risks of practicing real estate law can be costly, but they don’t have to be. With FCT helping you manage your risk, and three layers of affordable and effective protection, you can close every deal with confidence.

Learn more about which of our E&O suite of products are right for your practice and how to sign up today.

*E&O Complete offers coverage for up to three claims per year and $10,000 in coverage, with a $90,000 lifetime limit.

Insurance by FCT Insurance Company Ltd. Services by First Canadian Title Company Limited. The services company does not provide insurance products. This material is intended to provide general information only. For specific coverage and exclusions, refer to the applicable policy. Copies are available upon request. Insurance brokerage services by FCT Insurance Services Inc. Some products/services may vary by province. Prices and products/services offered are subject to change without notice.

®Registered Trademark of First American Financial Corporation.